The Potential Economic Effects of Trump’s Tariffs and Trade War

The period between February 1 and April 2, 2025, marks only the beginning of what increasingly appears to be a broader and intensifying trade conflict. The rapid succession of tariffs, retaliatory measures, and threats of further economic action, suggest that the situation remains fluid and highly volatile. As of the publication of this article, global trade dynamics are evolving at a pace that makes long-term predictions difficult.

The current conflict echoes the U.S.-China trade war of 2018, a major confrontation that began when the Trump administration imposed tariffs on Chinese goods. This trade dispute severely disrupted global supply chains and resulted in a significant decline in U.S. exports to China.

U.S. Tariff Policies and Rationale

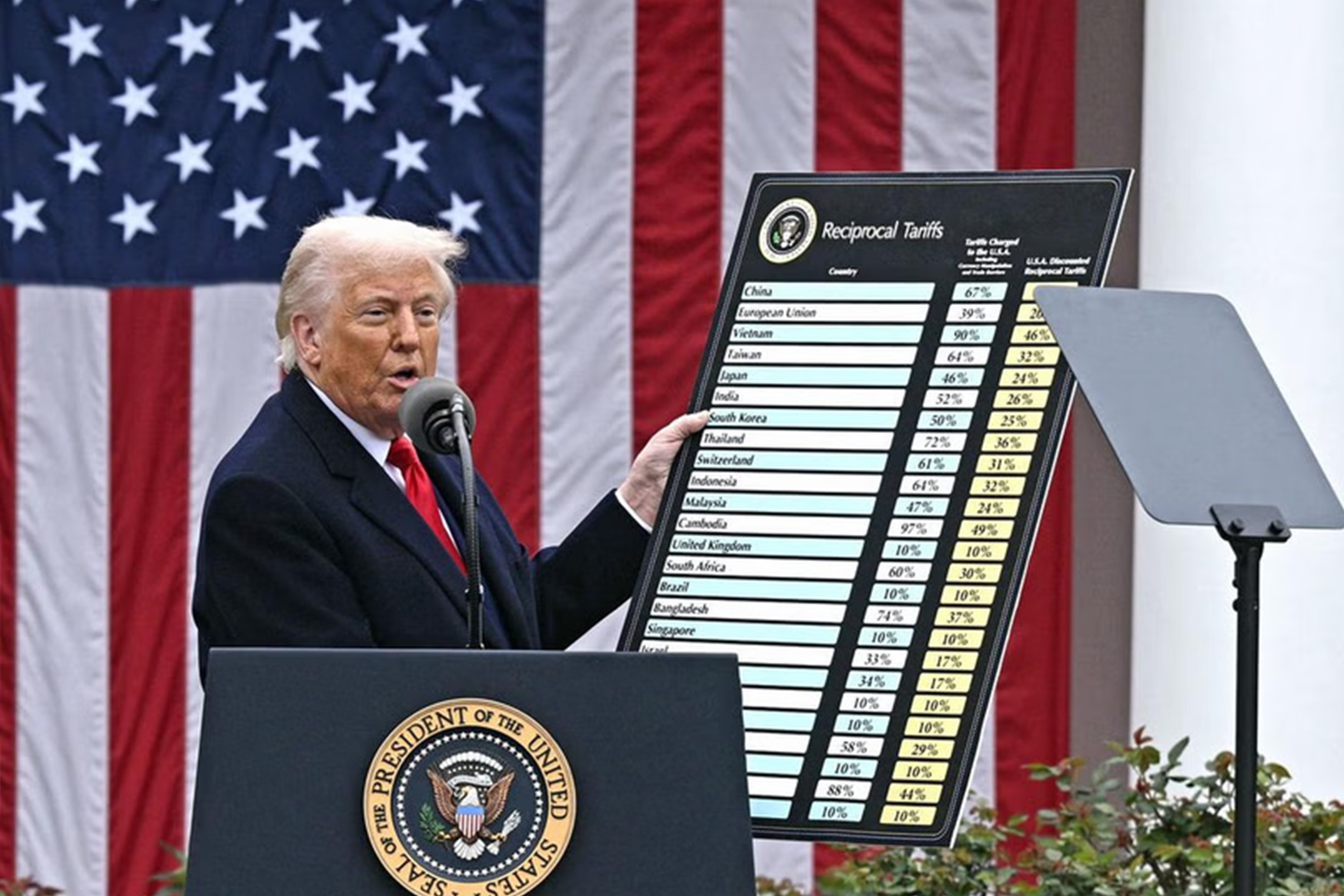

On February 1, 2024, President Donald Trump imposed significant tariffs on the United States largest trading partners: Canada, China, and Mexico. U.S. importers now face a 25 percent tax on goods from Canada and Mexico. The Trump administration justified these measures as a necessity to limit illegal migration and drug trafficking from these countries. Hence, they aimed to use these tariffs as leverage to compel these countries to take stronger actions against illegal activities and to enhance boarder security.

Canada and Mexico: U.S. importers now face a 25% tariff on goods from these countries, although energy products from Canada are subject to a lower rate of 10%.

China: Imports from China are subject to a 10% tariff, effective immediately.

These tariffs have had immediate economic and diplomatic repercussions, straining relationships with key trading partners and causing fluctuations in the stock market.

Impact on the U.S. Economy

Nearly half of all U.S. imports come from Canada, China, and Mexico. However, analysis by Bloomberg Economics shows that the new tariffs could reduce overall U.S. imports by 15 percent. While the Washington D.C. based Tax Foundation estimates that the tariffs will generate around $100 billion per year in extra federal tax revenue, they could also impose significant costs on the broader economy: disrupting supply chains, raising costs for businesses, eliminating hundreds of thousands of jobs, and ultimately driving up consumer prices.

Certain sectors in the U.S. economy will be particularly affected, mainly the automotive, energy, and food industries. For example, gas prices could surge by as much as 50 cents per gallon in the Midwest, as Canada and Mexico supply over 70 percent of the U.S. crude oil imports. The automotive sector is also at risk, as the U.S. imports nearly half of its auto parts from Canada and Mexico. A 25 percent tariff on these countries will increase production cost for U.S. automakers, potentially adding up to $3,000 to the price of some of the 16 million cars sold in the U.S. annually.

Additionally, grocery prices could rise, as Mexico provides more than 60 percent of U.S. vegetable imports and nearly half of all fruit and nut imports.

Effects on Canada and Mexico

Both Canada and Mexico are heavily reliant on trade with the United States.

More than 80 percent of Mexico’s exports—such as cars, machinery, fruits, vegetables, and medical equipment—are sent to the U.S. These exports represent about 15 percent of total U.S. imports.

The economic impact of a 25 percent tariff could be severe for Mexico, potentially slashing its GDP by 16 percent, with the auto industry suffering the most. Mexico exports nearly 80 percent of the cars it produces to the U.S., which amounts to 2.5 million vehicles annually.

Mexico’s energy sector is also vulnerable, as the U.S. imports about 60 percent of Mexico’s petroleum exports, much of which is crude oil for U.S. refineries. These tariffs could raise fuel prices in both countries, straining their economies.

Canada, similarly, faces significant challenges. Nearly 70% of Canada’s exports are sold to the U.S., with 80% of its oil exports going to American markets. Tariffs on energy products are expected to strain Canada’s economy, especially given its dependence on the U.S. market.

Effects on China

While China is less dependent on the U.S. market than Canada and Mexico, the 10 percent tariff could have an impact. Over the past two decades, China has gradually reduced dependence on trade in its economy, now accounting for about 37 percent of its GDP, down from over 60 percent in the early 2000s, offer some resilience.

In recent years, U.S.-China trade has slowed, particularly in industries affected by prior tariffs, such as auto parts and semiconductors. As a result, China has increased trade with other nations, including the European Union, Mexico, and Vietnam, softening the impact of additional tariffs. The 10 percent tariff on Chinese goods will likely have a reduced effect due to these adjustments.

Potential Repercussions and Retaliation

The tariffs could lead to further currency depreciation in the affected countries, which may mitigate some of the tariffs’ effects.

For example, a weakened yuan has already helped Chinese producers maintain their global competitiveness.

Similarly, the Mexican peso has depreciated by about 30 percent since April,

and the Canadian dollar has fallen by 8 percent since September. These currency shifts could help offset some of the tariff impacts.

In retaliation, countries like Canada, China, and Mexico are likely to impose their own tariffs on U.S. goods. Mexico, for instance, has already suggested this possibility, and the U.S.-Mexico-Canada Agreement (USMCA) would likely allow such measures.

This isn’t the first-time retaliation has occurred; in 2018, Mexico and Canada imposed retaliatory tariffs on U.S. goods after Trump’s steel and aluminum tariffs, costing the U.S. approximately $15 billion in exports. Similarly, U.S. farm exports to China dropped by $20 billion when China retaliated against U.S. tariffs.

Retaliatory tariffs would likely affect U.S. manufacturers, particularly those in states like New Mexico, Texas, Ohio, and Maine, where exports to Mexico and Canada are vital, such as semiconductor chips, auto parts, and metal products, which could face reduced demand as a result of tariffs.

In conclusion, while Trump’s Administration tariffs reflect a shift towards protectionism, with the goal of reducing trade deficits and strengthening domestic industries, the broader economic consequences could be severe for both the U.S. and its trading partners.

While the short-term revenue benefits and industry protection may be realized, rising consumer prices, economic slowdowns, and job losses in export-dependent sectors could outweigh these gains.

Moreover, the situation remains fluid. New tariffs are being announced, retaliations are unfolding, and economic pressures are mounting. Whether these policies will achieve their intended objectives or spiral into a trade war with economic repercussions remains uncertain.

The global economic landscape is being reshaped at an unprecedented pace, and the outcomes are increasingly difficult to foresee.