We deliver local knowledge backed by global strength.

With presence across the continents, we enable our member firms to deliver services that are locally relevant and globally aligned with international standards.

Our Network

Our Network

Insights

Insights

Business Insights providing executives with straightforward and strategic perspectives on key challenges: reshaping business models, addressing climate change and sustainability, and cultivating trust amidst rapid technological advancements.

All Insights

Services

Services

Our collaborative and transparent service portfolio includes assurance, business advisory, tax compliance and planning, risk assessment, and technology services. We prioritize integrity, objectivity, and confidentiality. With personalized strategies, we excel in meeting diverse client needs through a client-centric and proactive approach.

All Services

Industries

Industries

At PA Global, we stand as your reliable partner in navigating today’s complex and evolving business landscape. Our team of seasoned professionals brings deep industry expertise and a commitment to delivering tailored, forward-thinking solutions that empower organizations to grow sustainably and operate with resilience.

All Industries

Fraud Risk Isn’t Pressure or Opportunity. It’s Rationalization.

24 APR 2026

Assurance

Management

Risk

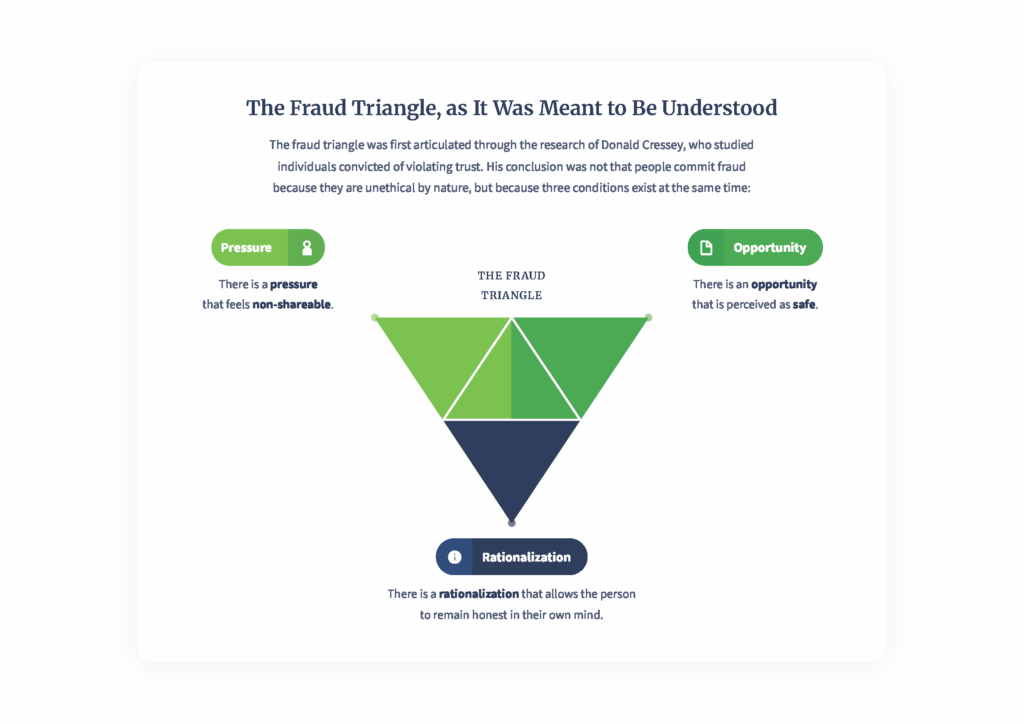

When organizations think about fraud risk, they usually focus on pressure and opportunity. Targets. Incentives. Weak controls. System access.

What they underestimate, almost every time, is rationalization.

Not because it is rare, but because it is reasonable.

The most dangerous fraudster is not the desperate one, or even the greedy one. It is the person who believes, sincerely, that what they are doing is justified.

Pressure may create the motivation. Opportunity may make the act possible. But rationalization is what makes the behavior acceptable to the person committing it. Without rationalization, the act cannot continue.

This is why rationalization sits quietly at the center of the triangle, often unnoticed, yet decisive.

Rationalization as the Quiet Accelerator

Rationalization is often treated as a secondary factor in fraud, a psychological explanation applied after misconduct is uncovered.

In reality, it is the engine.

Pressure may trigger the first step;

Opportunity may allow it to happen; but

Rationalization is what allows misconduct to continue, expand, and normalize.

Cressey observed that individuals did not see themselves as criminals. They saw themselves as good people facing temporary exceptions. That insight remains painfully relevant today.

What Rationalization Sounds Like in Real Life

Rationalization rarely sounds criminal. It sounds practical, temporary, even responsible.

“I’ll fix it next quarter” is how timing issues become permanent distortions. The intent is not to deceive forever, but to delay reality. Once results are issued, reversing them becomes harder. Each reporting period requires a larger adjustment. What began as timing quietly turns into fabrication.

“Everyone does it” is one of the most corrosive justifications. Ethics shift from principles to peer behavior. If misconduct appears normal, resistance starts to feel naïve rather than ethical. This is how entire teams, and sometimes entire departments, drift together.

“The company owes me” often appears when promotions are delayed, bonuses are cut, or loyalty goes unrewarded. The individual reframes misconduct as compensation and fraud becomes a form of self-correction rather than theft.

When people say, “Regulators do not understand our reality,” rationalization moves from individual to institutional. Rules are no longer questioned because they are unethical, but because they are seen as unrealistic. Compliance becomes performative, and violations feel intellectually defensible.

When Ethics Become Conditional

The critical insight is simple and uncomfortable: fraud accelerates when ethics become conditional.

- Conditional on performance pressure;

- Conditional on financial stress;

- Conditional on strategic importance;

- Conditional on seniority;

- Conditional on crisis.

In such environment, people stop asking whether something is right and start asking whether it is acceptable under the circumstances. Once ethics depend on context, rationalization no longer feels like an excuse; it feels like judgment.

Why Small Breaches Do Not Stay Small

Organizations often tolerate minor deviations because they appear immaterial, such as a single override, one exception, or an undocumented workaround. However, rationalization compounds far faster than any financial misstatement.

Each tolerated breach lowers internal resistance, signals implicit approval, reduces fear of consequences, and makes the next breach easier.

Over time, misconduct stops feeling like misconduct and begins to feel like how things are done here, which is how small, seemingly defensible decisions turn into systemic failure.

Leadership’s Uncomfortable Role

Rationalization does not emerge in a vacuum. It is shaped, often unintentionally, by leadership behavior.

It thrives when results are rewarded without scrutiny of how they were achieved, when ethical concerns are acknowledged but postponed, when high performers are protected from consequences, and when policies exist but enforcement is selective.

This is why ethical culture cannot be delegated to training sessions or signed declarations. Professional standards issued by the International Ethics Standards Board for Accountants (IESBA) requires professional accountants to comply with five fundamental principles, integrity, objectivity, professional competence and due care, confidentiality, and professional behavior, which together form the ethical foundation of the profession. Within this framework, fraud is not merely a technical misstatement or a regulatory breach; it is, by definition, a violation of integrity and professional behavior. IESBA makes this clear, emphasizing that integrity is demonstrated through actions and consistency rather than statements of intent, because people watch what is tolerated far more closely than what is written.

The Real Risk Signal

The most dangerous warning sign is not an anomaly in the data. It is hearing rationalizations spoken calmly, confidently, and repeatedly without challenge, because by the time someone feels the need to justify their actions, the ethical line has already been crossed.

Fraud does not begin with criminals. It begins with good people explaining to themselves why the rules do not apply, just this time.

Organizations that want to prevent fraud must listen less for violations and more for justifications. Because when people believe they are right, controls no longer matter.

Sources:

- Association of Certified Fraud Examiners – Report to the Nations

- Committee of Sponsoring Organizations of the Treadway Commission (COSO) – Fraud Risk Management Guide

© 2026 PA Global. All rights reserved.